ESI full form is Employees’ State Insurance.

It is a self-financing social security and health insurance scheme for Indian workers, managed by the Employees’ State Insurance Corporation (ESIC), under the Ministry of Labour and Employment.

If you’ve ever checked your salary slip and noticed “ESI deduction,” you’re not alone. Many employees see it every month but aren’t fully sure what it actually means.

Let’s clear the confusion.

Understanding the ESI full form isn’t just about knowing three words — it’s about knowing your rights, benefits, and financial protection as an employee in India.

Now, let’s break this down in simple, practical terms so you know exactly how ESI works, who qualifies, and why it matters.

What Is ESI? (Simple Explanation)

ESI stands for Employees’ State Insurance, a government-backed scheme designed to provide financial and medical support to employees earning below a specified wage limit.

In other words, it acts as a safety net.

Whenever an insured employee faces:

- Illness

- Maternity

- Workplace injury

- Disability

- Death (in certain cases)

the ESI scheme offers financial compensation and medical benefits.

Therefore, ESI is not just a deduction — it’s protection.

Origin and Legal Background of ESI

The ESI scheme was introduced under the Employees’ State Insurance Act, 1948, making it one of India’s earliest social security laws after independence.

It is administered by the Employees’ State Insurance Corporation (ESIC), which operates under the Ministry of Labour and Employment, Government of India.

Why Was It Introduced?

Post-independence, India needed a structured welfare system for industrial workers. As a result, ESI was created to:

- Provide healthcare access

- Offer wage compensation during sickness

- Protect workers from financial instability

Over time, the scheme expanded across multiple states and industries.

How Does ESI Work?

The ESI scheme works through shared contributions from both employers and employees.

Current Contribution Rates

| Contributor | Contribution Rate |

|---|---|

| Employer | 3.25% of wages |

| Employee | 0.75% of wages |

(Rates as per latest standard contribution structure.)

Because both parties contribute, the scheme remains self-financing.

Who Is Eligible for ESI?

Not everyone automatically qualifies. Eligibility depends on salary and organization type.

Basic Eligibility Criteria

- Employee earning up to ₹21,000 per month (₹25,000 for persons with disabilities)

- Working in a company registered under the ESI Act

- Company employs 10 or more employees (may vary by state)

If your salary exceeds the limit after enrollment, you continue to receive benefits until the contribution period ends.

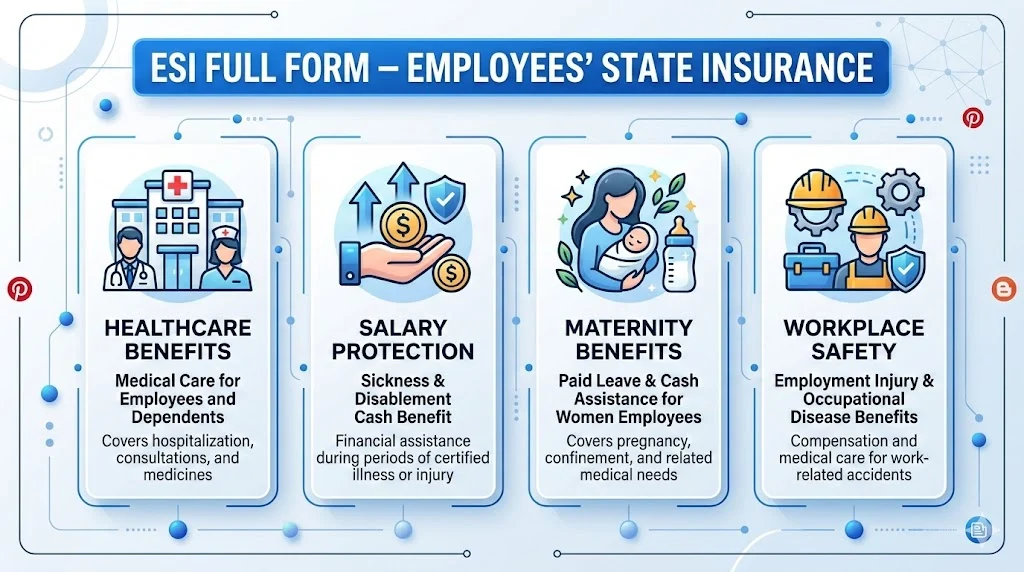

Key Benefits of ESI

One of the main reasons ESI is important is its wide range of benefits. Let’s look at them clearly.

1. Medical Benefits 🏥

- Free medical treatment for insured employee

- Coverage for dependents

- Hospitalization and specialist care

2. Sickness Benefit 🤒

- 70% of wages during certified medical leave

- Payable for up to 91 days in a year

3. Maternity Benefit 👶

- Paid maternity leave

- Full wage compensation for eligible period

4. Disablement Benefit

- Compensation for temporary or permanent disability

- Work-related injury coverage

5. Dependents’ Benefit

- Financial support to family in case of employee’s death due to employment injury

6. Funeral Expenses

- Lump-sum financial support for funeral costs

Clearly, ESI goes far beyond basic insurance.

Real-Life Example of ESI in Action

Imagine this:

Rahul works in a manufacturing unit and earns ₹18,000 per month. One day, he suffers a workplace injury and cannot work for two months.

Because he is enrolled under ESI:

- His hospital bills are covered

- He receives wage compensation

- His family doesn’t face financial strain

Without ESI, the situation could have been financially devastating.

Tone and Usage of “ESI” in Different Contexts

Unlike emotional phrases, ESI is mostly used in formal and administrative settings.

1. Professional Tone

“Your ESI contribution has been deducted this month.”

2. Informational Tone

“Employees earning below ₹21,000 are eligible for ESI benefits.”

3. Concerned Employee Tone

“Why is ESI being deducted from my salary?”

Because it relates to employment and law, the tone is typically neutral and professional.

ESI vs EPF – What’s the Difference?

Many people confuse ESI with EPF. However, they serve different purposes.

| Feature | ESI | EPF |

|---|---|---|

| Full Form | Employees’ State Insurance | Employees’ Provident Fund |

| Purpose | Health & social security | Retirement savings |

| Managed By | ESIC | EPFO |

| Salary Limit | ₹21,000/month | No strict upper limit |

| Type | Insurance | Savings scheme |

In short:

- ESI = Health + emergency financial protection

- EPF = Long-term retirement savings

Alternate Meanings of ESI

Although Employees’ State Insurance is the most common meaning in India, ESI can have other meanings in different fields:

- Economic Sentiment Indicator (Finance)

- Electrospray Ionization (Chemistry)

- Extended Spectrum Inhibitor (Medical research context)

However, in employment and payroll contexts, ESI almost always refers to Employees’ State Insurance.

Professional Alternatives and Related Terms

Depending on context, you might also encounter:

- Social Security Scheme

- Government Health Insurance

- Employee Welfare Program

- Labour Insurance Scheme

Still, ESI remains the legally recognized term in India.

Common Mistakes About ESI

Let’s clear up some misunderstandings.

❌ “ESI is a tax.”

No, it’s a contribution-based insurance scheme.

❌ “Only private companies offer ESI.”

Incorrect. Any registered company meeting eligibility criteria must provide it.

❌ “You lose benefits if salary increases.”

Not immediately. Benefits continue until the contribution period ends.

Frequently Asked Questions (FAQ)

1. What is the full form of ESI?

ESI stands for Employees’ State Insurance.

2. Who is eligible for ESI?

Employees earning up to ₹21,000 per month in registered establishments qualify.

3. Is ESI mandatory?

Yes, for eligible employees working in covered establishments.

4. How much is deducted for ESI?

Employees contribute 0.75% of wages, while employers contribute 3.25%.

5. Can I use ESI for my family?

Yes, dependents are covered under medical benefits.

6. What happens if my salary exceeds ₹21,000?

You continue coverage until the current contribution period ends.

7. Is ESI better than private insurance?

It depends. ESI is cost-effective and mandatory for eligible workers, while private insurance offers broader flexibility.

8. Can I withdraw ESI amount?

No, ESI is not a savings account. It provides benefits during emergencies.

Why ESI Is Important Today

In today’s unpredictable economic environment, healthcare expenses can rise suddenly. Because of this, ESI acts as a critical financial cushion for millions of workers.

Moreover, it ensures that lower-income employees receive structured medical and income protection support.

Conclusion: Key Takeaways About ESI Full Form

- ESI full form is Employees’ State Insurance

- It is a government-backed social security scheme

- Both employer and employee contribute

- Provides medical, maternity, disability, and dependents’ benefits

- Mandatory for eligible employees in covered establishments

Ultimately, ESI is not just a payroll deduction — it’s a protective framework designed to safeguard workers and their families.